.png)

Behavioral Finance: The Variable That Impacts Returns Most

In wealth management, we often prioritize technical analysis, asset allocation, and tax strategies. However, the data suggests that these factors are often secondary to investor behavior. Understanding the psychology of decision-making is a requirement for maintaining a successful long-term strategy.

What is the "Behavior Gap"?

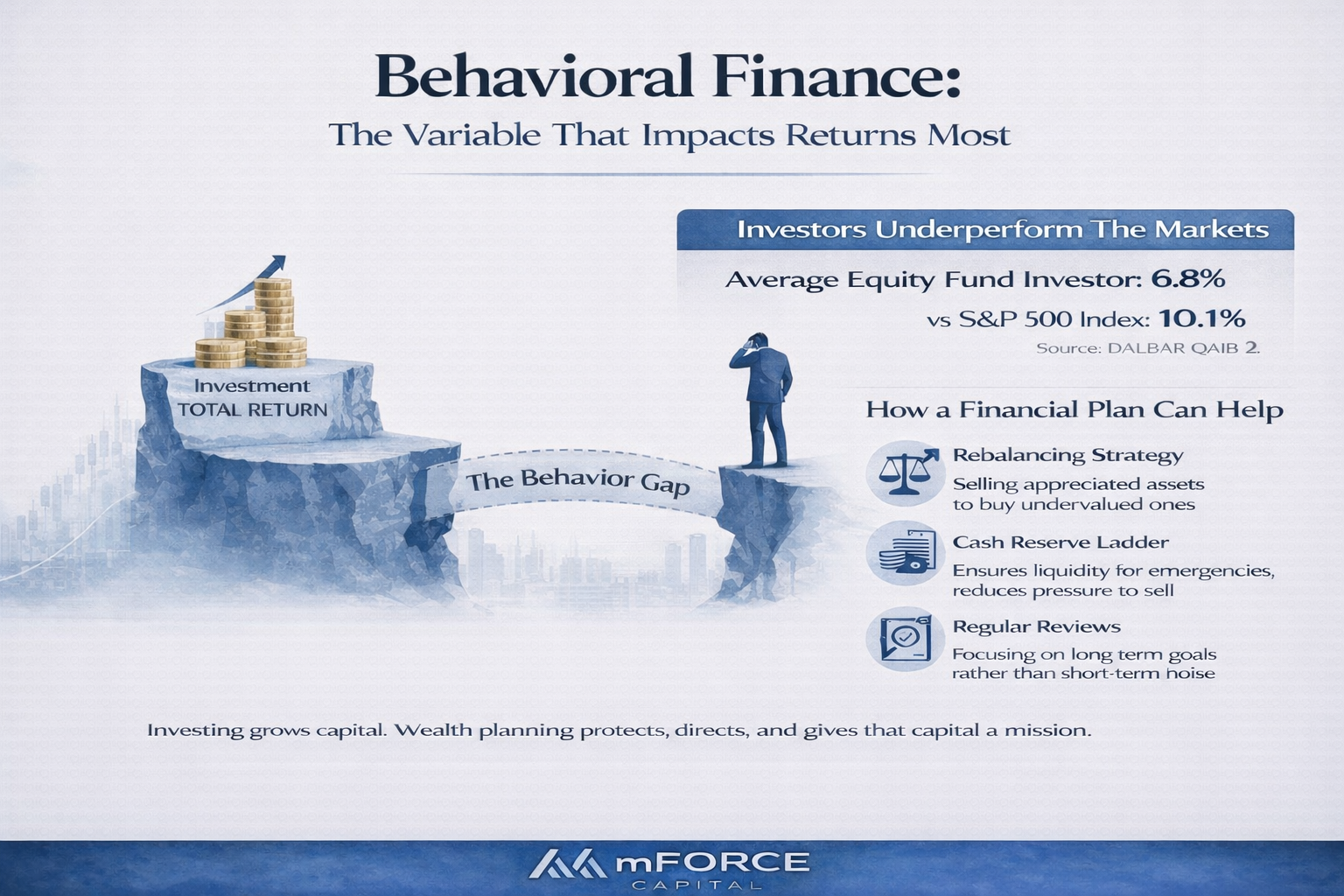

The "Behavior Gap" is the difference between the total return of an investment and the actual return realized by the investor. This gap exists because individuals frequently buy or sell based on emotional triggers rather than the fundamentals of their financial plan.

Common Behavioral Biases in Wealth Management

Even high-net-worth investors with significant business experience are susceptible to cognitive biases. Recognizing these patterns is the first step toward mitigating their impact:

- Loss Aversion: Research indicates that the psychological pain of a loss is roughly twice as potent as the pleasure of a gain. This often leads to "panic selling" during temporary market corrections to avoid further discomfort.

- Recency Bias: The tendency to over-weight recent events when making future predictions. If the market has been up for three years, investors often take on too much risk; if it has been down for three months, they often become overly conservative.

- Confirmation Bias: Seeking out news or opinions that support our existing views while ignoring contradictory evidence. This can lead to a skewed perception of market reality.

- Availability Heuristic: Placing too much importance on information that is "available" or top-of-mind, such as sensationalist financial news headlines, rather than long-term historical data.

The Math of Discipline

Fact Check: According to the 2025 DALBAR Quantitative Analysis of Investor Behavior (QAIB), the average equity fund investor consistently underperforms the S&P 500. This underperformance is rarely due to the investments themselves but rather the timing of entries and exits. Over a 30-year period, the cost of emotional decision-making can result in a significantly smaller portfolio value.

A Systemic Solution: The Financial Plan as a Framework

A structured financial plan serves as a logical "circuit breaker." It moves decision-making from an emotional context to a systematic one. This includes:

Rebalancing Protocols: Automatically selling assets that have performed well to buy assets that are currently undervalued.

- Cash Reserve Ladders: Ensuring that short-term liquidity needs are met, which reduces the pressure to sell long-term assets during a downturn.

- Risk Mitigation: Ensuring your family and business are protected from liabilities.

- Regular Strategy Reviews: Focusing on your specific goals and "Traction" metrics rather than daily market movements.

- Takeaway: Successful investing is a function of temperament as much as it is intelligence. By establishing a disciplined framework, you can minimize the impact of behavioral biases and improve your long-term outcomes.

Articles You May Also Find Helpful

The roadmap to financial success

A step-by-step PDF that outlines the key financial milestones individuals and families should aim for, including wealth preservation, estate planning, and legacy building.